From Awareness to Architecture: Why Governance Integration Is Private Equity's Next Valuation Lever

Mid-market PE firms no longer need convincing that sustainability risk matters. The issue now is whether they can prove it is governed across the investment lifecycle in a way that stands up to LP scrutiny, buyer diligence, and exit pressure.

April 2026

Governance is now the real test

Private equity has moved past the awareness phase. Most serious mid-market firms are no longer debating whether climate and sustainability risk matters. The real issue now is governance.

Can you show, in a way that survives serious scrutiny, how that risk is actually governed across the investment lifecycle?

That is the new test. And in many firms, it is still where the weakness sits.

A GP-level ESG policy is easy enough to produce: a few pages in the fund documents, some language in LP reporting, a set of principles on the website. None of that is especially difficult. What is difficult is building a governance model that connects those commitments to what actually happens inside portfolio companies, in board discussions, in value creation plans, and in exit preparation.

That is the shift. This is no longer mainly about awareness, disclosure, or intent. It is about architecture.

And in private equity, architecture has a direct bearing on value.

Where private equity firms are still exposed

This is where many firms still fool themselves.

At GP level, the language is often well developed. The policy exists. The investment team knows how to talk about climate and sustainability risk. LP communications are polished. The annual ESG update says all the right things.

One level down, inside the portfolio, the picture often changes.

Board papers contain little or no documented challenge on climate-related risk. Ownership is vague. Reporting is inconsistent. What was raised in diligence fades after close. Sustainability sits in the background, acknowledged but not embedded in the governance rhythm of the business.

That is the real gap.

Private equity’s strength has always been control and influence. But that control comes with a governance burden. If a GP is going to make claims about sustainability risk, it needs to be able to show how those claims are being translated into actual oversight at portfolio company level.

Too often, they are not.

What starts as a GP commitment ends up stuck in limbo. It is discussed at acquisition, deferred during the first 100 days, diluted during the hold period, and rediscovered under pressure when the business is preparing for exit.

That is not integration. That is drift.

And by the time the gap becomes visible in diligence, it is usually much harder to fix properly.

The most common weakness is not policy at GP level. It is the failure to translate that policy into portfolio company governance.

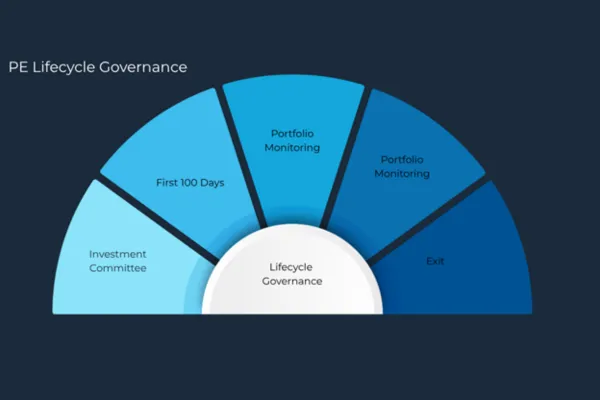

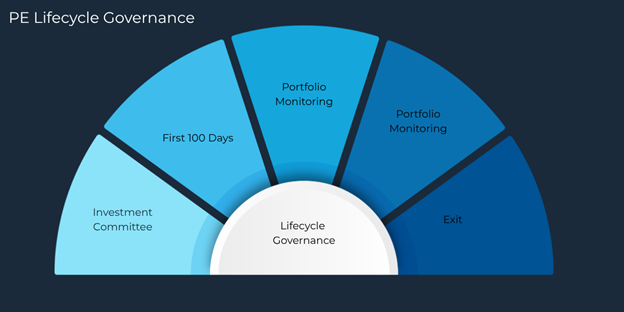

Where the gap becomes visible

Governance in PE is not abstract. You see it, or fail to see it, at specific points in the deal cycle.

Investment committee

This is where governance integration should begin. If climate and sustainability-related risk appears only as a footnote or a soft ESG comment in the investment memo, it is not shaping the investment thesis in any serious way.

The question is simple: are governance maturity, transition exposure, and regulatory readiness being assessed in a structured way at entry, or not?

First 100 days

This is where good intentions usually go to die.

If governance integration is not built into the post-acquisition value creation plan, it tends to get pushed into a vague “phase two” that never really arrives. The first 100 days set the operating rhythm for the hold period. If the governance work is not there early, it is unlikely to become systematic later.

Portfolio monitoring

This is another common failure point. Many firms still rely on inconsistent ESG questionnaires or ad hoc updates that create the appearance of oversight without much substance behind them.

The real test is whether there is a consistent way to monitor governance maturity across the portfolio, with reporting that shows actual oversight activity, ownership, challenge, and follow-through. The ESG Data Convergence Initiative (EDCI), now used by hundreds of GPs and LPs, has standardised the data side of this conversation. But data without governance discipline is reporting, not oversight.

Board oversight

This is where the evidence has to exist.

Do portfolio company boards have clear ownership of climate and sustainability-related risks? Is there documented challenge? Is there any sign the board has done more than acknowledge the issue?

A board that is aware of a risk but does not oversee it in a structured way does not have governance. It has awareness.

Exit preparation

This is where the market gets a vote.

Can the firm show a buyer, lender, or insurer a clear evidence trail connecting GP commitments to portfolio execution? Can it demonstrate that governance has been active, documented, and sustained through the hold period?

If not, the problem shows up at exactly the worst moment: when valuation is most sensitive and time is shortest.

If governance integration does not show up at these decision points, it is not shaping outcomes where it matters.

Governance integration should be visible throughout the investment lifecycle, not rediscovered at exit.

Why this is now a valuation issue

This is the part the market is getting faster at understanding.

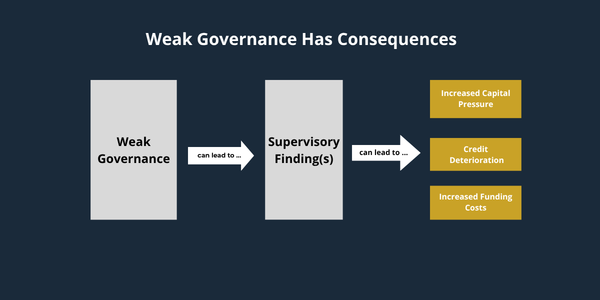

Weak governance around climate and sustainability risk is no longer just a policy weakness. It is a valuation issue.

At entry, weak governance assessment creates blind spots in the investment thesis. Risks tied to transition exposure, regulatory readiness, insurability, or operational vulnerability may not be properly identified or priced.

You can see this most clearly in certain value-add real estate and infrastructure-adjacent strategies. Assets that looked attractive in 2021–2022 are now exposed to tightening energy performance standards, changing insurance appetite, and more conservative lender requirements. GPs that treated energy and transition risk as an ESG side-note at entry are now adjusting exit cases or capex plans under time pressure.

During the hold period, governance gaps create drag. Reporting is inconsistent. Operating partner engagement becomes less effective. The business misses the chance to build the evidence base that will later support the exit story.

There is also a cost of capital angle. ESG-linked ratchets in subscription lines and unitranche facilities are now common in the mid-market. Those margin moves may be modest — often in the 5 to 15 basis point range — but they are tied to specific governance and data KPIs. A GP that cannot track and evidence them uniformly is, at best, leaving pricing on the table.

At exit, the consequences are more direct. Buyers, lenders, and insurers are asking harder questions. ESG-focused vendor due diligence is now standard at the upper mid-market and moving steadily into core mid-market deals. Where governance evidence is weak:

diligence takes longer,

management gets pulled into remediation instead of buyer meetings,

assumptions become harder to defend, and

pricing pressure follows.

It is not unusual to see processes extend by 60 to 90 days when governance gaps are uncovered late. In the current market, 90 days can mean a different financing environment at close.

That is how value leaks.

The firms that handle this well tend to be stronger in four areas:

Sharper entry decisions, because governance and transition risks are assessed properly at the start.

Stronger hold-period oversight, because expectations are clear and reporting is consistent.

More credible value creation narratives, because they are backed by documented governance, not broad claims.

Better exit readiness, because the diligence file has been built over time rather than assembled in a rush.

In some deals, this is no longer a differentiator. It is part of the price of entry.

Weak governance increasingly shows up in pricing, financing, diligence friction, and exit readiness.

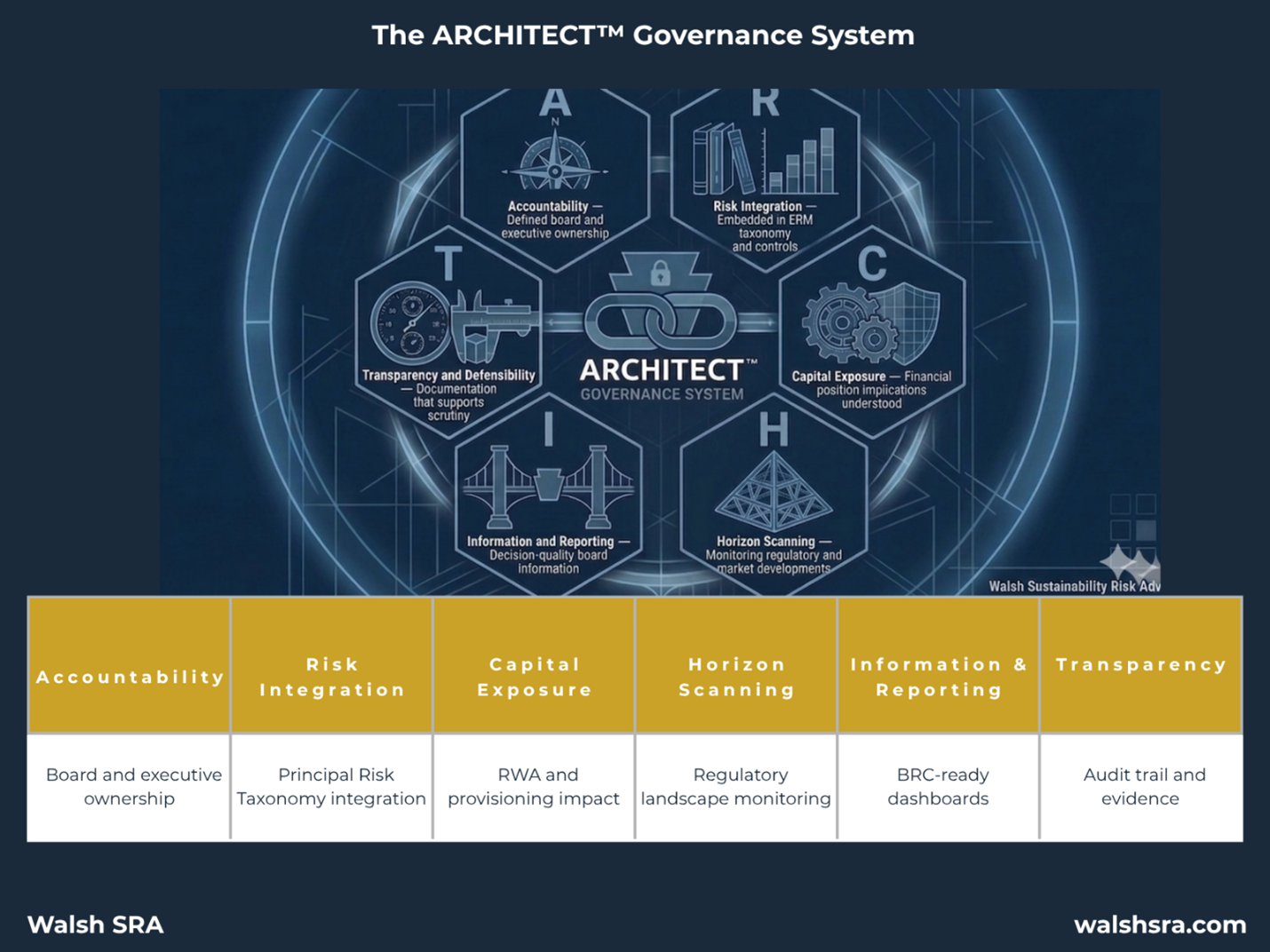

The ARCHITECT™ Governance System

I originally developed the ARCHITECT™ Governance System for regulated financial institutions, where supervisory pressure forced earlier maturity in governance architecture. The underlying question turned out to be identical in private equity: Can you evidence that a financially material risk is being governed, or only that it is being acknowledged?

I built ARCHITECT™ because I could see the same pattern repeating. Firms had policy language, but not governance architecture. They could describe their intentions, but they could not always show how governance was operating across the portfolio in a way that would survive serious scrutiny. That is the gap the system is designed to address.

In a private equity context, the six ARCHITECT™ pillars translate into practical governance requirements across the deal cycle:

A: Accountability

Who owns the risk, specifically? Not in general terms. Named accountability at GP level, within deal teams and operating partner structures, and at portfolio company board level.R: Risk Integration

Is climate and sustainability-related risk embedded in investment decisions, portfolio oversight, and exit preparation, or treated as a separate ESG track?C: Capital Exposure

Can the firm connect governance quality, or the lack of it, to financial performance, financing conditions, insurability, and exit value?H: Horizon Scanning

Is there a disciplined way to track LP expectations, regulatory developments (including SFDR and CSRD in Europe), and sector transition pressures across the portfolio?I: Information and Reporting

Does the GP receive decision-useful reporting that reflects real governance activity, or just annual narrative updates?T: Transparency and Defensibility

Can the firm produce a documentation trail that connects GP commitments to portfolio-level execution and shows that governance has actually happened?

The goal is straightforward: move sustainability governance out of the policy file and into the operating model.

The ARCHITECT™ Governance System translates sustainability ambition into a governance model that can withstand scrutiny.

Mid-market PE firms need to stop hiding behind good intentions

Most firms are not getting this wrong because they do not care. They are getting it wrong because they still think good intentions, a credible policy, and some ESG reporting are enough.

They are not.

The market is asking harder questions now. LPs have moved beyond policy language into how governance actually shows up in IC papers, 100-day plans, and board minutes. European regulation, particularly SFDR and the evolving CSRD timetable, has raised the disclosure bar for funds marketing into the EU and for larger portfolio companies within scope. Buyers and lenders are looking more closely at governance quality during diligence. And portfolio companies, especially in the lower and core mid-market, often do not have the internal infrastructure to deal with this on their own.

That means the burden falls back on the GP.

This is where mid-market firms need to be honest with themselves. Being mid-market does not remove the problem. In some ways it sharpens it. You still face scrutiny, but often with less internal infrastructure and less room to recover if a gap shows up late.

That is why delay is a mistake.

If sustainability governance disappears after diligence and reappears only during exit prep, that is not a process. It is a warning sign.

Good intentions do not substitute for governance discipline.

Five questions every GP should ask now

Before the next investment committee or portfolio review, ask five direct questions:

Are we assessing climate and sustainability-related governance risk in a structured way at entry, or are we still relying on generic ESG diligence?

Do our first 100-day plans include governance integration milestones, or are we quietly postponing the work?

Do our portfolio company boards have clear, documented ownership of climate and sustainability-related risks?

Are we getting consistent reporting across the portfolio that reflects actual oversight activity, not just annual ESG narrative?

Could we demonstrate real governance integration to a sophisticated buyer, lender, or LP conducting diligence today?

If those questions produce hesitation, the governance gap is already there.

Closing

The governance gap will be priced. The only question is whether the GP prices it first, or the buyer does.

In this market, the firms that treat sustainability governance as part of how they create, protect, and realise value and not as a reporting obligation will be the ones that move through LP reviews and sell-side diligence from a position of strength rather than catch-up.

The firms that wait will end up doing the same work later, under pressure, in front of an audience.

_______________________________________________________

Not sure how your governance framework would stand up under LP review, regulatory examination, or sell-side diligence? The ARCHITECT™ Governance Maturity Assessment gives mid-market private equity firms a practical starting point. Over two to three weeks, it shows where governance is strong, where it is exposed, and what needs to change.

_______________________________________________________

Author bio

Brendan Walsh is the founder of Walsh SRA and creator of the ARCHITECT™ Governance System. He brings more than 30 years of global executive leadership in regulated financial services, including senior roles at American Express across the US, Europe, and Asia, as well as advisory experience with regulated institutions including the UK's Office of Gas and Electricity Markets (OFGEM). He holds a master's degree in sustainability from Harvard University and is credentialed by GARP in both Sustainability and Climate Risk (SCR) and AI Risk. Walsh SRA advises mid-tier financial institutions and private equity firms on governance frameworks for climate and sustainability-related financial risk.